Here’s what you should do.

Millions of Youth South Africans lack the financial literacy necessary to make it into adulthood.Here’s what’s wrong, who it mostly affects,and what you can do.

Maybe nobody ever sat you down and explained how interest rates work in school. No one told you what a credit

score is. No one told you why retirement savings matter. If that sounds familiar, you’re not alone and it’s not your

fault.

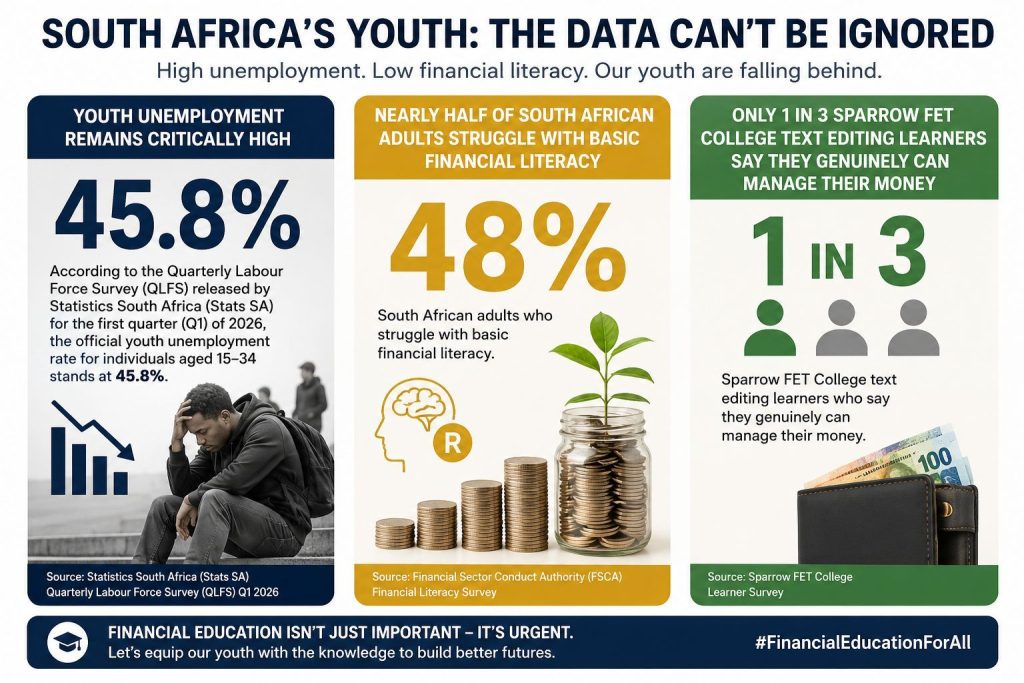

All the evidence from national surveys point to the conclusion: a large proportion of South African youth lack

the financial knowledge that will enable them to make wise choices about saving, debt, budgeting, investing and

long-term planning.

WHY IS THIS?

It’s not a simple thing. It’s a combination of educational gap economic history and social pressures that compound.

GAPS IN THE EDUCATION SYSTEM- Financial education is not an obligatory subject.

Economic and Management Sciences (EMS) does cover some theory, but practical money skills are seldom taught.

SOCIO-ECONOMIC INEQUALITY- Millions of young South Africans are raised in homes where their parents have limited financial literacy, zero bank accounts and no culture of savings.

Predatory LENDING (loan practice that is abusive, deceptive and unfair)- Young people are also frequently targeted by buy-now-pay-later schemes and high-fee credit products before they have the tools to critically evaluate them.

PRESSURE OF BLACK TAX- Support from extended family and social pressure to spend can make saving feel impossible, which discourages long-term financial planning.

LIMITED ACCESS TO BANKING- Despite the growth of mobile banking, most rural and township youth remain under banked, limiting their exposure to formal banking systems.

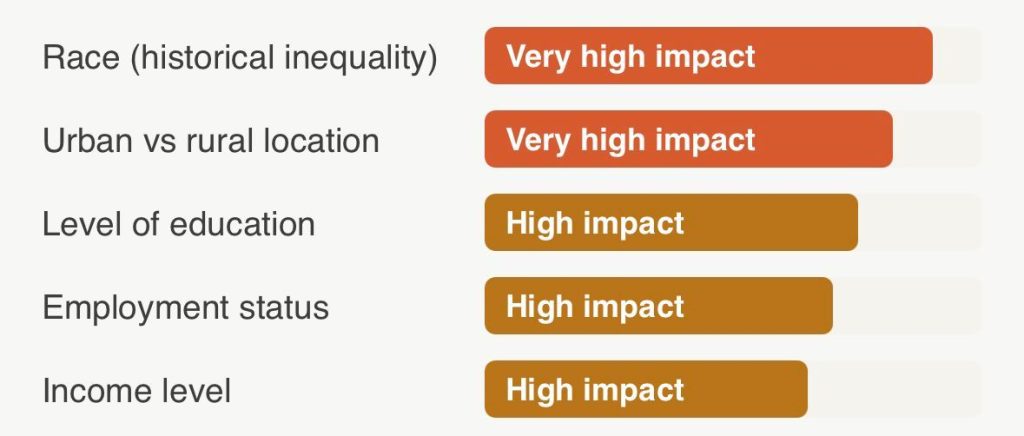

Who gets hit hardest?

Research published in the South African Journal of Economic and Management Sciences found that financial literacy in South Africa is not evenly distributed.

Youth from disadvantaged backgrounds are disproportionately impacted because informal markets dominate in many communities, schools often don't offer practical financial education, and parents may lack financial literacy themselves.

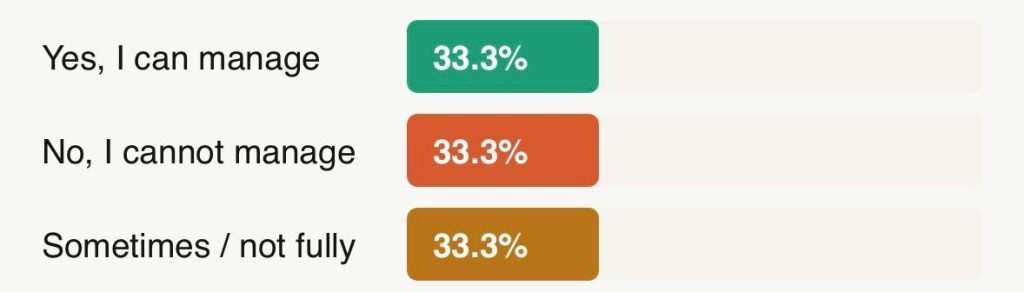

What do young people actually know? A survey among

learners at Sparrow FET College under the Text Editing faculty gave an honest picture of where financial confidence stands:

Two-thirds of respondents said they are not good at managing money.

The implications of this are more than just personal stress. Moreover, high unemployment means that many young people grow up without steady income, familiarity with credit or exposure to banking and investing systems, leaving them more vulnerable to predatory lending, financial fraud, excessive debt and poor long-term decisions.

5 things you can do today!

- Track all your expenses for a week. Awareness is the first step to control.

- Open a free savings account (many banks have zero-fee youth accounts). Even R50 a month builds the habit.

- Know what your credit score means before you apply for any credit. It follows you for a lifetime.

- Be sceptical of buy-now-pay-later deals, (e.g MoreTyme). If you can't pay cash, ask yourself if you really need it now.

- Use free financial education resources- they exist and they are made for you.

Where to learn more, for free?

The good news: banks and regulators are responding. These resources are freely

available to all South Africans:

FNB Fincents- FNB's new digital financial education hub that is designed to close SA's literacy gap, with resources for all communities.

FSCA Consumer Education- The Financial Sector Conduct Authority runs national

financial literacy campaigns and offers consumer guidance.

22seven (Old Mutual)- A free budgeting and savings app that links to your accounts and helps you track spending in real time.

Capitec Bank Academy: Money Academy capitecbank.co.za